Mobile Home Insurance in Texas

Find Cheap Mobile Home Insurance Quotes in Texas

Mobile home insurance ensures you're protected if your home is damaged. The insurance is technically optional, but many mobile home communities and mortgage lenders in Texas require homeowners to have this coverage. Mobile home insurance policies are customizable, and rates vary, so you'll want to compare quotes from several Texas insurance companies before purchasing.

Mobile home insurance rates in Texas

The cost of mobile home insurance in Texas depends on several factors, but coverage is often more expensive than typical home insurance.

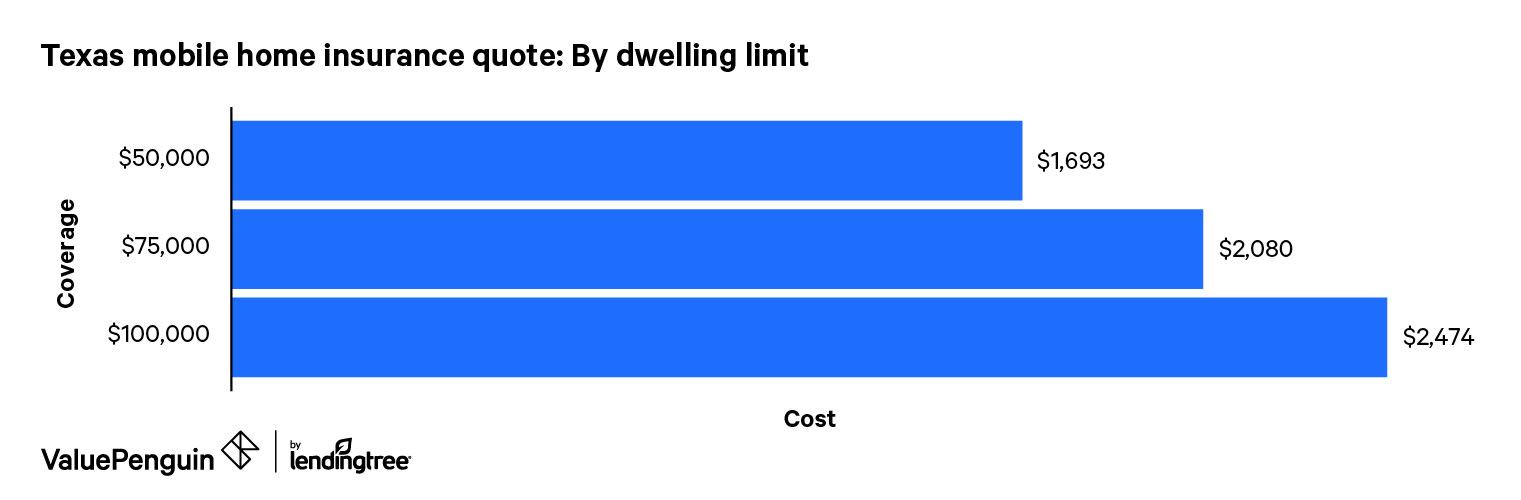

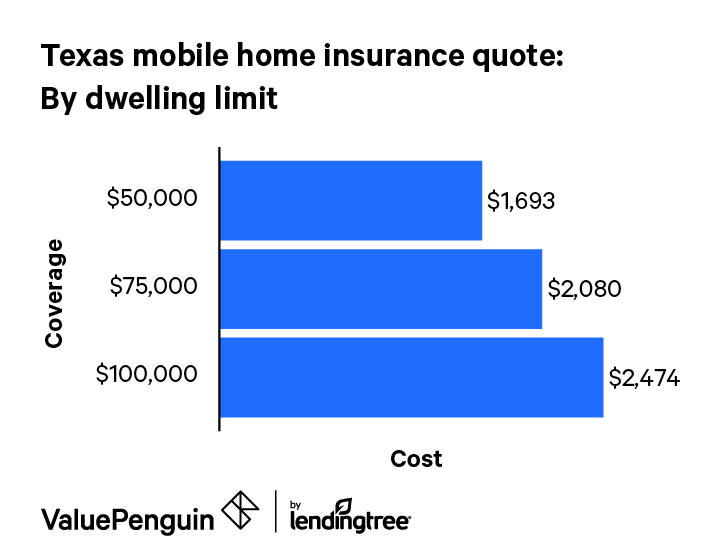

Texas's mobile home insurance rates depend on where your home is located, how old it is and the coverage you need. In addition, one of the largest rate factors is your dwelling coverage limit. Below are sample quotes for mobile home insurance in Houston, Texas, for multiple dwelling coverage limits.

Find Cheap Mobile Home Insurance Quotes in Texas

The best way to get cheap mobile home insurance in Texas is to shop around and compare quotes. Some companies may provide quotes online, but be prepared to call others on the phone.

As noted, expect to pay more for mobile home insurance than you would for a standard homeowners insurance policy in Texas. That's because mobile homes are more susceptible to damage, so they're insured at a higher cost.

Do I need mobile home insurance in Texas?

As with standard homeowners insurance, no law in Texas requires mobile home insurance. But most lenders do. Mobile home communities and parks also may require tenants to have insurance.

In Texas, a mortgage lender can require insurance but can't require that a borrower buy coverage that exceeds the replacement value of the home and its contents. The only way to definitely avoid getting mobile home coverage in Texas is to buy a manufactured home outright and place it on private property.

Regardless, you should get mobile home insurance for financial protection. Without it, you'd have to pay out of pocket for any damage that occurs. Repair costs covered by an insurance policy, such as a roof leak stemming from a tree falling on your home, can quickly add up, so it's best to have the safeguard that insurance provides.

Unique considerations: Texas mobile home insurance

Mobile home insurance policies typically cover wind and hail damage. But these may be excluded if you live near the coast, where homes are more susceptible to flood, wind and hail damage. If you're having trouble finding flood insurance in the private market, you could buy it through the National Flood Insurance Program, which allows homeowners to buy federally backed flood insurance.

For wind and hail, you have the option of getting coverage from a private insurance company or through the Texas Windstorm Insurance Association (TWIA). The TWIA was formed in 1971 to provide wind and hail insurance to people who live along the coast and don't qualify for private coverage.

The average wind and hail insurance policy from TWIA costs $2,000 per year. Keep in mind that the TWIA only offers wind and hail coverage, meaning you'll still need to buy a mobile home insurance policy.

Counties where mobile homes are eligible for TWIA wind and hail coverage

- Aransas

- Brazoria

- Calhoun

- Cameron

- Chambers

- Galveston

- Jefferson

- Kenedy

- Kleberg

- Matagorda

- Nueces

- Refugio

- San Patricio

- Willacy

Mobile homes located within the limits of the following cities and east of Highway 146 are also eligible for TWIA wind and hail coverage:

- La Porte

- Morgan's Point

- Pasadena

- Seabrook

- Shore Acres

What does mobile home insurance in Texas cover?

Mobile home insurance offers similar coverage to a homeowners insurance policy. They provide:

- Coverage for the physical structure

- Replacement of personal items

- Liability protection

Most Texas mobile home insurance companies allow you to customize your policy through endorsements, or policy add-ons. The add-ons provide extra coverage that doesn't come standard with a homeowners policy.

Most mobile home insurance companies in Texas allow you to set custom coverage limits.

- Dwelling coverage: Mobile home insurance in Texas provides coverage for permanent structures attached to the home. For instance, if a car crashes into your living room, your insurance company will pay to repair damage to the walls, roof and an attached deck.

-

Personal property: A mobile home insurance policy also covers your personal belongings, whether they're damaged or stolen. For example, furniture damaged by a fire would be covered after you pay the deductible.

- Liability protection: This coverage offers you protection when a guest suffers an injury while on your property. For instance, if your neighbor is hit by a falling ceiling fan in your home,, your insurance company would provide protection for any legal or medical fees, up to your coverage limit.

- Other structures: Most mobile home insurance policies also include coverage for other free-standing structures on your property. For example, any damage to a toolshed or fence would be covered.

-

Additional living expenses: If your home is uninhabitable due to a covered loss, this coverage would compensate you for the costs of living away from home, such as a hotel room.

Filing a mobile home insurance claim in Texas

According to Texas law, your insurance company must acknowledge your claim within 15 days of receiving it.

Once the company has all the info they need from you, they have 15 business days to accept or deny your claim. However, the deadline may be extended if a major disaster is taking place.

A company can take up to 45 days to make a decision on your claim, as long as they've sent you a letter explaining the delay. If the insurance company doesn't meet the aforementioned deadlines, you can sue them for the claim amount, interest and legal fees.

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.